Cheryl Knowlton: Hi everybody. Cheryl Knowlton, Dynamite Productions here with my favorite sidekick-

Clay Johnson: Hi again.

Cheryl Knowlton: Clay Johnson, with Castle and Cooke Mortgage. So today let’s talk about the fed and interest rates. They are historically low, again.

Clay Johnson: They are so, so good. And it’s interesting because we were in a big … with the federal reserve, the challenges. People hear that in the news and they think that,  “Hey, this has a direct correlation with my 30-year mortgage.” And it actually doesn’t. So it affects car loans, it affects home equity lines of credit, kind of your short-term. It’s really the overnight lending rate that that affects which has a direct impact on the prime interest rate. Now there can be a trickle-down effect, but right now what we’re looking at … so we just saw the first cut that we’ve seen since they just raised everything.

“Hey, this has a direct correlation with my 30-year mortgage.” And it actually doesn’t. So it affects car loans, it affects home equity lines of credit, kind of your short-term. It’s really the overnight lending rate that that affects which has a direct impact on the prime interest rate. Now there can be a trickle-down effect, but right now what we’re looking at … so we just saw the first cut that we’ve seen since they just raised everything.

Things were doing good, they kind of gave us some raises for a while. We sat stagnantly and we just saw the first cut, I think it was eight years that we saw. So that is going to have a little bit of a trickle-down impact. Gives the markets a lot of confidence and they expect that over the next … well, between now and the end of the year, we’ll probably see two additional overnight lending rate cuts. But people say, “Okay, then what affects the longterm mortgages?” And there are two things. Number one, the thing that’s really helping us right now, cause we’re the lowest we’ve been in three years-

Cheryl Knowlton: In terms of the fixed rates?

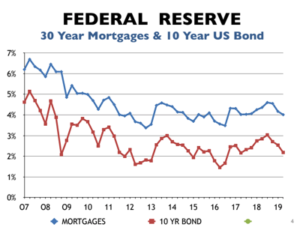

Clay Johnson: The 30 year fixed rates. And a lot of it’s the global uncertainty, it’s the trade war kind of between us and China. What’s happening as far as that’s concerned. Kind of the economic uncertainty, that drives a lot of activity into secure markets like mortgage-backed securities and treasury bonds. And the value of those goes up, the yields go down, the rates follow the yield. So whenever there’s kind of that economic uncertainty, we’re the smartest kids in the not so bright classroom sometimes-

Cheryl Knowlton: Great analogy.

Clay Johnson: We’ve done really well, so those secure investments with us have been really strong and it’s really helped the rate. So we’ve seen kind of the best of both worlds with the overnight lending rate, and the longterm rates are both doing phenomenal right now. And people say, “When is it worth it?” Well, for every 1% the rates go down, for the area median income, it’s going to raise your purchasing power about $20,000.

Cheryl Knowlton: Wow.

Clay Johnson: So yeah, it’s pretty cool.

Cheryl Knowlton: Yes.

Clay Johnson: And a lot of folks are taking advantage of the additional statements right now with rates being so low from where they’ve been on a historical level.

Cheryl Knowlton: That’s fantastic. So next time in our second episode, we’re going to talk about when is it advantageous for you and/or your clients to refinance. So come back to tomorrow’s episode and we’ll see you then.

Clay Johnson: Bye-bye.